Electronic Arts ( NASDAQ:EA ) had a rough month, with its share price falling 7.0%. However, the company’s fundamentals look pretty decent, and long-term financials are generally aligned with future market price movements. Specifically, we decided to examine Electronic Arts’ ROE in this article.

Return on equity, or ROE, is a key measure used to assess how efficiently a company’s management is using the company’s capital. In other words, it is a profitability ratio that measures the rate of return on the capital provided by the company’s shareholders.

Check out our latest analysis on Electronic Arts

How do you calculate return on equity?

The formula for ROE is:

Return on equity = Net income (from continuing operations) ÷ Equity

So, based on the above formula, the ROE for Electronic Arts is:

14% = US$1.1 billion ÷ US$7.5 billion (Based on trailing twelve months to December 2023).

“Return” refers to the company’s earnings over the past year. So, this means that for every $1 of its shareholder’s investment, the company generates a profit of $0.14.

Why is ROE important to earnings growth?

We have already established that ROE serves as an effective profit-generating measure of a company’s future earnings. Now we need to estimate how much profit the company is reinvesting or “holding back” for future growth, which then gives us an idea of the company’s growth potential. All else being equal, the higher the ROE and earnings retention, the higher the growth rate of a company compared to companies that do not necessarily have these characteristics.

Electronic Arts revenue growth and 14% ROE

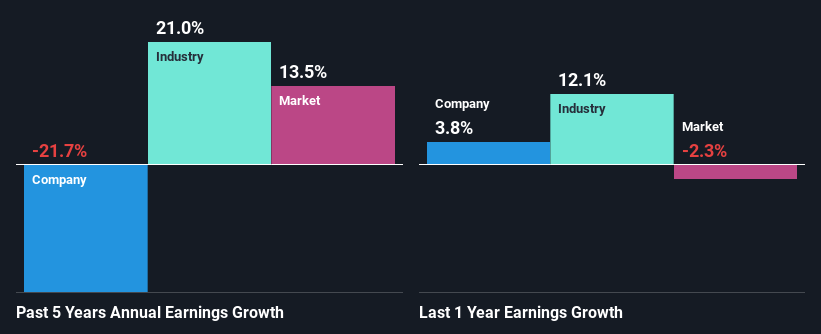

To begin with, Electronic Arts appears to have a respectable ROE. Even compared to the industry average of 14%, the company’s ROE looks pretty decent. For this reason, Electronic Arts’ five-year net income decline of 22% begs the question of why decent ROE has not translated into growth. Based on this, we believe that there may be other reasons that have not been discussed so far in this article that could be hindering the company’s growth. For example, it could be that the company has a high payout ratio or the business has allocated capital poorly, for example.

That being said, we compared Electronic Arts’ performance to the industry and were concerned to find that while the company has shrunk its earnings, the industry has grown its revenue at a rate of 21% over the same 5-year period.

The basis for valuing a company is largely related to its revenue growth. It is important for the investor to know whether the market has priced in the expected growth (or decline) of the company’s earnings. This then helps them determine whether the stock is set for a bright or dark future. What is EA worth today? The intrinsic value infographic in our free research report helps visualize whether EA is currently mispriced by the market.

Is Electronic Arts effectively using its retained earnings?

Electronic Arts’ low three-year average payout ratio of 22% (which suggests it retains the remaining 78% of its earnings) comes as a surprise when you combine it with shrinking earnings. The low payout should mean the company keeps most of its earnings and should therefore see some growth. So there may be other explanations in this regard. For example, the company’s business may be deteriorating.

In addition, Electronic Arts has paid dividends over a three-year period, suggesting that maintaining a dividend payout is preferred by management even though earnings are in decline. Existing analyst estimates suggest that the company’s forward payout ratio is expected to fall to 9.6% over the next three years. Accordingly, the expected decline in the payout ratio explains the expected increase in the company’s ROE to 27% over the same period.

Summary

Overall, Electronic Arts seems to have some positive aspects to its business. However, we are disappointed to see a lack of growth in earnings even despite a high ROE and high reinvestment rate. We believe that there may be some external factors that could have a negative impact on the business. Having said that, looking at current analyst estimates, we find that the company’s earnings growth rate is expected to see a huge improvement. To learn more about the latest analyst estimates for the company, see this preview of analyst estimates for the company.

Have feedback on this article? Concerned about content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article from Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts, using only an unbiased methodology, and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell shares and does not take into account your goals or your financial situation. We aim to provide you with long-term focused analysis driven by fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or quality materials. Simply Wall St has no position in the stocks mentioned.